Khyber Tobacco Company Financial Results

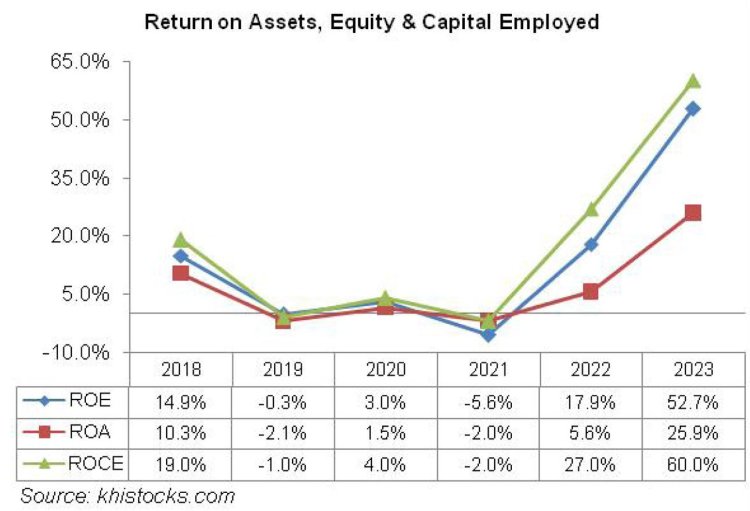

KHTC's top line has decreased twice since 2018—in 2019 and 2021. During these years, the company's financial results were similarly poor. The ensuing years are marked by growth, both top and bottom line, that is astounding.The company's margins had a sharp decline in 2019 and a rebound in 2020. But in 2021, the margins started to shrink once more. KHTC had a time of financial vibrancy and enthusiasm for the next two years, demonstrating an astounding turnaround in its margins.

Business Recorder

Business Recorder

In 1954, Khyber Tobacco corporation (PSX: KHTC) was established as a public limited corporation in Pakistan. The corporation does more than just re-dry tobacco; it also makes and markets cigarettes. The company's range also includes non-tobacco items including filter rods. In addition to growing its distribution network in Eastern Europe, South and West Africa, Central and South Asia, and the Middle East, KHTC is a major player in the Pakistani market.

Pattern of Ownership

There are 6.92 million outstanding shares of KHTC as of June 30, 2023, and 1178 shareholders own them. With a 91 percent investment in KHTC, the local public is the company's largest shareholder, followed by insurance firms with a 3.46 percent stake. Three percent of KHTC's shares are held by foreign investors, while 1.11 percent are held by directors, their spouses, and their minor children. Other kinds of shareholders split up the remaining ownership.

Historical Results (from 2018 to 22)

KHTC's top line has decreased twice since 2018—in 2019 and 2021. During these years, the company's financial results were similarly poor. The ensuing years are marked by growth, both top and bottom line, that is astounding.The company's margins had a sharp decline in 2019 and a rebound in 2020. But in 2021, the margins started to shrink once more. KHTC had a time of financial vibrancy and enthusiasm for the next two years, demonstrating an astounding turnaround in its margins. Below is a full performance evaluation for each of the years that are being considered.

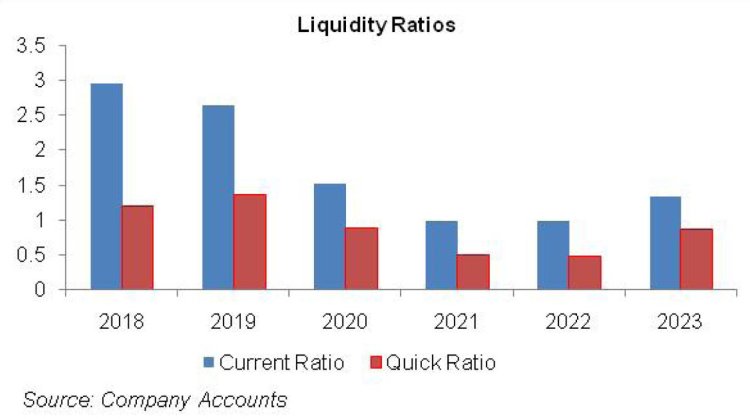

KHTC's net sales fell 5% in 2019 compared to the previous year. Local sales plummeted by 16 percent year over year to Rs 2102 million, but export sales showed an amazing surge of almost 42 times to reach Rs 235.76 million. Low volumetric sales in the cut tobacco and cigarette categories were the cause of the sales decline, although re-dried tobacco off-take increased to 1.42 million kilogrammes in 2019 from 0.166 million kilogrammes in 2018, a 754 percent year-over-year increase (refer to the sales volume table). The growing cost of sales reduced gross profit by 64 percent in 2019 and reduced the GP margin to 17 percent from 44 percent the year before.The year-over-year decline in administrative expenses was primarily caused by a decrease in trade debt write-offs and a decrease in rent. In contrast, significant marketing of re-dried tobacco, customs, clearing, and freight on export sales, as well as sales staff training, resulted in a 33 percent year-over-year increase in distribution expenses in 2019. As a result, operational profit in 2018 was Rs. 268.47 million, while operating loss in 2019 was Rs. 29.47 million. Due to a high discount rate and increased borrowing to meet working capital requirements, finance costs climbed by 382% in 2019. KHTC reported a financial loss of Rs. 38.27 million in 2019 as a result, down from a net profit of Rs. 199.87 million in 2018. The company recorded loss per share of Rs.7.96 in 2019 versus EPS of Rs.41.57 in 2018.

2020 saw a 71% increase in KHTC's topline year over year. This resulted from high off-take in each of the three categories—cut tobacco, re-dried tobacco, and cigarettes (refer to the sales volume table). Despite COVID-19, local and foreign sales saw a significant upturn in 2020. The 17 percent GP margin did not change. 2020 saw a 13% annual increase in administrative expenses, mostly due to rising payroll costs. 2020 saw a 21% increase in distribution expenses year over year as a result of increased export freight, customs, clearing, and sales personnel training. This resulted in an OP margin of 3% and an operating profit of Rs. 62.74 million in 2020. Finance cost slid by 57 percent in 2020. KHTC registered net profit of Rs.38.54 million in 2020 with NP margin of 2 percent and EPS of Rs.8.02.

After a brief period of reprieve, the topline was once more negatively impacted in 2021, falling by 34% year over year. This followed a sharp decline in the off-take of tobacco that had been re-dried. The other two categories' dispatches somewhat grew, but they were unable to have any effect on the top line (see to the sales volume table).

2021 saw a more than 50% decline in export sales as a result of the weak demand for tobacco from Pakistan on the global market. Sales costs plummeted by 30% annually, resulting in a 48% reduction in gross profit in 2021. In 2021, the GP margin decreased to 14 percent. Reduced export revenue spared the business from export freight, customs, and clearing costs. This, together with little marketing and promotion efforts, caused the distribution expense to decrease by 46% on an annual basis. In 2021, administrative costs decreased by 8% on an annual basis as well. KHTC reported an operational loss of Rs26.93 million in 2021 despite making focused efforts to control operating expenses. In 2021, despite a low discount rate for the year, finance costs increased by 177% year over year. This was the result of a massive hike in current liabilities during the year. This produced a major dent on the bottomline which posted a net loss of Rs68.65 million in 2021 with loss per share of Rs.14.28.

KHTC posted a staggering 103 percent year-on-year growth in its topline in 2022 on the back of increase in off-take across categories particularly re-dried tobacco (see the table of sales volume). The company also undertook rigorous initiatives during the year which boosted its export sales. The depreciation of Pak Rupee also played its part in keeping the net sales robust. GP margin flew up to 33 percent in 2022 while gross profit multiplied by 388 percent. Customs, clearance and freight on export sale expanded the distribution expense by 115 percent year-on-year in 2022. Administrative expense also grew in line with inflation and also because the workforce grew from 372 employees in 2021 to 460 employees in 2022 which drove up the payroll expense. KHTC posted operating profit of Rs.532.76 million in 2022 which translated into OP margin of 22 percent. Finance cost also grew owing to higher borrowings and record high discount rate during the year. The net profit for the year stood at Rs.315 million culminating into NP margin of 13 percent and EPS of Rs.65.62 in 2022.

Among all the years under review, 2023 stands out due to a spectacular 202 percent increase in net sales and a more than 500 percent increase in net profit year over year. This was the outcome of a startling rise in sales volume in all categories, especially in re-dried tobacco (refer to the sales volume table).

Export sales registered a whopping increase over 400 percent and stood at 55 percent of KHTC’s gross sales in 2023 versus 27.6 percent in 2022. Higher proportion of export sales also buttressed the GP margin amid Pak Rupee depreciation. KHTC’s GP margin climbed to 37 percent in 2023. Administrative expense hiked by 59 percent year-on-year in 2023 mainly on account of higher payroll expense as the number of employees grew to 598 in 2023. Distribution expense surged by 149 percent in 2023 primarily due to higher custom, clearance and freight on export sales. Research expense and promotion expense also spiked in 2023.

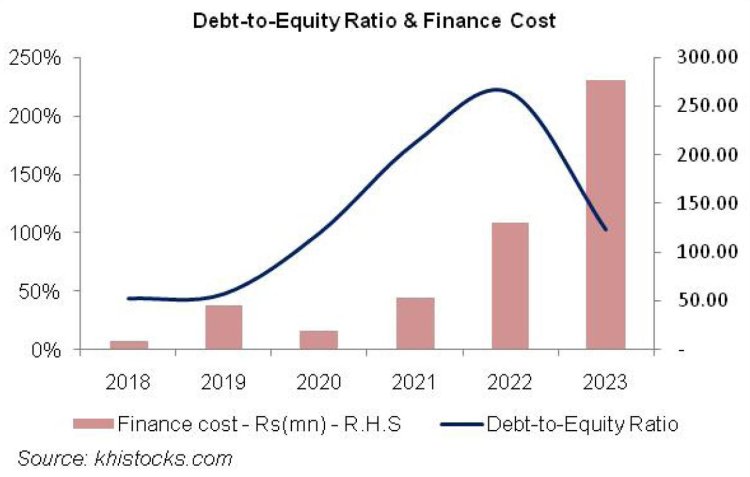

There was a significant rise in impairment loss on trade debts in 2023 which clocked in at Rs.61.96 million, up over 22.5 times year-on-year. Operating profit widened by 309 percent in 2023 with OP margin rising up to 29 percent. Other expense escalated by 484 percent in 2023 on account of profit related provisioning, FED and sales tax written offduring the year. However, other expense was absorbed by hefty other income which grew by 940 percent in 2023 on account of exchange gain. Finance cost mounted by 112 percent in 2023 on account of higher discount rate although borrowings notably dived down in 2023 as evident in KHTC’s debt-to-equity ratio (see the graph). The company posted 534 percent year-on-year growth in its net profit which stood at Rs.1998.40 million in 2023 with EPS of Rs.288.68 and NP margin of 27 percent – the highest among all the years under consideration.

KHTC's net sales in the first quarter of FY24 fell sharply by 68 percent year over year, thus the company didn't start the year off well. The corporation attributes the fall in sales to the ineffective implementation of the Track & Trace system, which allows the illicit and counterfeit cigarette sector to thrive at the expense of legitimate market participants. Additionally, export sales decreased significantly in 1QFY24, resulting in a gross loss of Rs. 47.35 million as opposed to a profit of Rs. 633.55 million in the same period the previous year. Due to marketing initiatives to increase local sales in the face of weak export sales, as well as inflation, administrative and distribution expenses increased by 14% and 9%, respectively. In comparison to its operational profit of Rs. 507.37 million in 1QFY23, KHTC had an operating loss of Rs. 188.83 million in 1QF24. In 1QFY24, finance costs fell 68% year over year. Comparing the first quarter of FY24 to the same time in FY23, the company's net profit was Rs. 405.55 million, whereas its net loss was Rs. 249.76 million. In 1QFY24, the loss per share was Rs. 36.08, while in 1QFY23, the EPS was Rs. 84.36.

Future Prognosis

The tobacco industry's net revenues may be negatively impacted by the increase in sales tax and federal excise duty on cigarettes, but market participants have responded by raising prices sharply. Nonetheless, the price hike will allow the black market for cigarettes to expand.Local sales are probably going to rise once the Track & Trace system is fully implemented. The company's liquidity position, however, would be in jeopardy if the declining trend continues since it has remained heavily dependent on its export sales.